The Global Aerostructures Market is a cornerstone of the aerospace and defense industry, encompassing the design, manufacturing, and assembly of all external and internal load-bearing components of an aircraft. These critical elements include the fuselage, wings, empennage (tail section), nacelles (engine casings), and flight control surfaces. This market's trajectory is intrinsically tied to global air traffic volume, defense spending cycles, and relentless pressure for fuel efficiency.

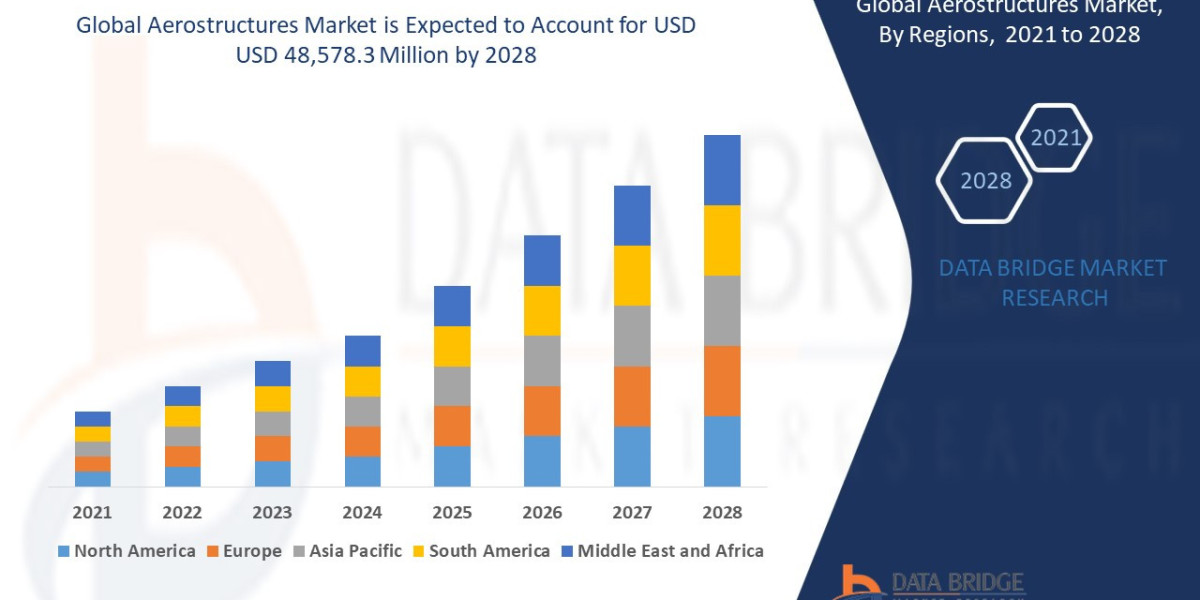

The aerostructures market will reach at an estimated value of USD 48,578.3 million by 2020 and grow at a CAGR of 5.60% in the forecast period of 2021 to 2028.

Market Dynamics and Growth Drivers

The Aerostructures Market is valued in the tens of billions of U.S. dollars and is experiencing a healthy, long-term expansion. After recovering from pandemic-related disruptions, the market is projected to grow at a steady Compound Annual Growth Rate (CAGR) typically ranging between $6.5\%$ and $7.5\%$ through the next decade.

Key Drivers Propelling Market Growth:

Record Commercial Aircraft Backlogs: The primary driver is the massive, years-long backlog of aircraft orders held by major original equipment manufacturers (OEMs) like Boeing and Airbus. Driven by rising global passenger traffic, the need for fleet expansion, and the replacement of older, less fuel-efficient aircraft, this backlog provides stable, multi-year revenue visibility for aerostructure suppliers.

The Imperative for Fuel Efficiency and Lightweighting: Strict environmental regulations and the operational need to reduce fuel consumption (the largest operating cost for airlines) compel manufacturers to prioritize weight reduction. This drives the transition from traditional aluminum alloys to advanced composite materials (like Carbon Fiber Reinforced Polymers - CFRP) in components like wings, fuselages, and empennages.

Increased Defense Budgets and Modernization: Geopolitical tensions and modernization programs in North America, Europe, and Asia-Pacific are leading to sustained high defense spending. This fuels demand for advanced military aerostructures for next-generation fighter jets, transport aircraft, and the rapidly growing segment of Unmanned Aerial Vehicles (UAVs).

Emergence of Advanced Air Mobility (AAM): The nascent but high-growth sector of electric Vertical Take-Off and Landing (eVTOL) vehicles and Urban Air Mobility (UAM) is creating demand for entirely new, ultra-lightweight aerostructures that utilize innovative composite and additive manufacturing techniques.

Market Segmentation: Materials and Components

The market's complexity is defined by the components built and the materials used to meet demanding performance requirements.

By Component:

Fuselage (Largest Revenue Share): The main body structure of the aircraft, which houses passengers, cargo, and crew. It maintains the largest revenue share due to its size and structural complexity.

Wings (Fastest Growing Segment): Driven by the adoption of large, high-aspect-ratio composite wings designed to improve aerodynamic performance and fuel efficiency.

Empennage: The tail section (vertical and horizontal stabilizers) crucial for flight stability.

Nacelles and Pylons: Structures surrounding the engine, which are critical for temperature resistance and propulsion efficiency.

https://www.databridgemarketresearch.com/reports/global-aerostructures-market

By Material:

Alloys and Superalloys (Current Volume Leader): Still dominate the market volume, particularly high-strength aluminum and titanium alloys, used where high strength, fracture toughness, and cost-efficiency are critical (e.g., landing gear components, legacy aircraft structures).

Composites (Fastest Growing Segment): Includes CFRP and glass fiber composites. This segment is growing rapidly, driven by the superior strength-to-weight ratio and fatigue resistance necessary for new generation aircraft (e.g., Boeing 787, Airbus A350).

By Platform:

Commercial Aircraft (Dominant Share): Holds the largest market share, led by narrow-body aircraft production (like the A320neo and 737 MAX families).

Military Aircraft: Includes fighters, bombers, and transports, characterized by high-specification materials and complex, custom designs.

Advanced Air Mobility (AAM) / UAVs: The segment projected to exhibit the highest CAGR, focusing on high-volume production of composite structures for small electric vehicles.

Regional Dynamics

North America: Dominates the global market share, owing to the strong presence of major OEMs (e.g., Boeing) and Tier-1 suppliers, along with significant defense modernization programs.

Asia-Pacific (APAC): Expected to be the fastest-growing regional market. Growth is driven by the region's rapidly expanding middle class, booming air passenger traffic, massive fleet expansions by regional airlines, and government initiatives to develop domestic aerospace and defense manufacturing capabilities (e.g., in China and India).

Browse More Reports:

Global Urinary pH Modifiers Market

Global Wearbale Injectors Market

Global Clinical Trial Packaging and Labelling Market

Global COVID-19 Drug Delivery Devices Market

Global On Premise Time Tracking Software Market

Global Para-Virtualization Market

Global Rental Leasing On-Demand Transportation Market

Global Fluorinated Oil Market

Global Soft Touch Polyurethane Coatings Market

Global UltraViolet-C (UVC) Disinfection Products Market

Global Window Sensors Market

Global Wood Pellet Heating Systems Market

Global Cosmetic Implants Market

Global Full-field Digital Mammography (FFDM) Market

Global Mini Light-Emitting Diode (LED) Market

Conclusion

The Global Aerostructures Market is positioned for a sustained period of growth, defined by the twin objectives of rate readiness and material transition. The immediate future is secured by the massive commercial aircraft backlog, forcing the supply chain to focus intensely on increasing production rates while maintaining stringent quality control. However, the long-term future is fundamentally focused on sustainability and weight reduction, cementing the shift towards advanced composite materials and Additive Manufacturing (3D printing) for complex parts. As new platforms like eVTOLs mature and military modernization continues, the aerostructures market will remain the technological core of the aviation industry, consistently redefining the boundaries of material science and manufacturing efficiency.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com