Executive Summary:

The Global Electronic Chemicals and Materials Market is a foundational industry that supplies the ultra-high purity substances essential for manufacturing all modern electronic components. This includes specialty gases, wet chemicals, silicon wafers, photoresists, and CMP slurries used in the fabrication of semiconductors, integrated circuits (ICs), and printed circuit boards (PCBs).

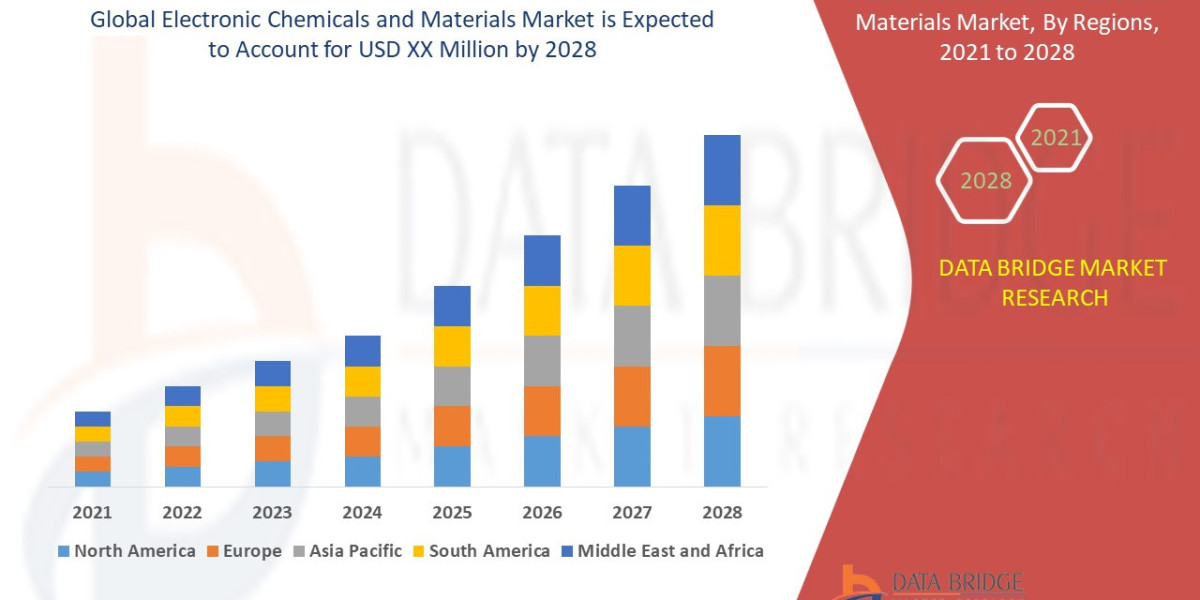

The core driver is the explosive demand for semiconductors across virtually all industries, fueled by 5G, IoT, AI, and Electric Vehicles (EVs). The Semiconductor and IC segment is the dominant application, with Silicon Wafers holding the largest revenue share by product. Asia-Pacific is the largest and fastest-growing regional market due to its dominant role in global electronics manufacturing.

The electronic chemicals and materials market is expected to witness market growth at a rate of 6.05% in the forecast period of 2021 to 2028.

Industry Overview: Segmentation and Critical Products

The market is highly specialized, categorized by the form, type of material, and its specific application in the manufacturing process.

Market Size and Growth Metrics (Estimated Range)

| Metric | Estimated Value (2024) | Projected CAGR | Forecast Period |

| Market Value (Current) | $\approx$ USD 67.35 Billion – 77.44 Billion | - | - |

| Projected CAGR | $\approx$ 5.5% – 6.2% | (Average) | Through 2032-2035 |

| Dominant Application | Semiconductors and Integrated Circuits (ICs) ($\approx 48\%$ share) | - | |

| Dominant Product Type | Silicon Wafers | - |

Key Market Segmentation

| Segmentation | Dominant Sub-Segment | Key Drivers |

| By Product Type | Silicon Wafers | Fundamental substrate for nearly all ICs; demand driven by capacity expansion. |

| Fastest Growing Product | Photoresists & Ancillaries | Critical for advanced lithography and chip miniaturization (EUV adoption). |

| By Form | Solid (Wafers, Substrates, PCB Laminates) | Highest revenue share due to high material cost of core components. |

| By Application | Semiconductors & ICs | Core application, driven by logic, memory, and advanced chip fabrication. |

| Fastest Growing Application | Displays (OLED, LED) | Rising adoption of high-efficiency displays in consumer electronics. |

| By End-User | Consumer Electronics | High volume demand from smartphones, PCs, and smart home devices. |

| By Region | Asia-Pacific (APAC) ($\approx 44.5\% - 69\%$ share) | Concentration of global Foundries (fabs), PCB, and electronics assembly in China, Taiwan, South Korea, and Japan. |

Analysis: Drivers, Challenges, and Emerging Trends

Key Market Drivers

Explosive Growth of the Semiconductor Industry: The market is directly tied to the exponential rise in semiconductor sales, fueled by applications like Artificial Intelligence (AI), Internet of Things (IoT), Cloud Computing, and 5G infrastructure. This drives intensive demand for ultra-pure chemicals for fabrication.

Technological Miniaturization and Scaling: The continuous push for smaller feature sizes (moving to sub-20nm nodes) and the adoption of advanced lithography technologies like Extreme Ultraviolet (EUV) drastically increases the complexity and purity requirements for materials such as photoresists, etchants, and CMP slurries.

Government Support and Supply Chain Resilience: Global initiatives (like the U.S. CHIPS Act and EU Chips Act) aim to regionalize and de-risk semiconductor supply chains. This massive investment in new domestic fabrication facilities globally creates an immediate, multi-year demand surge for specialized materials.

Automotive Electronics Revolution: The shift to Electric Vehicles (EVs) and autonomous driving systems significantly increases the semiconductor content per vehicle, boosting demand for reliable, high-performance materials in power management chips and sensors.

Advancements in Display Technology: The transition to OLED, QLED, and Micro-LED displays creates a strong market for specialized organic semiconductors, conductive polymers, and wet chemicals.

https://www.databridgemarketresearch.com/reports/global-electronic-chemicals-and-materials-market

Market Challenges and Restraints

High R&D and Capital Costs: Developing and manufacturing ultra-high purity chemicals, especially for advanced nodes, requires substantial capital investment in R&D and specialized, contamination-free production facilities.

Environmental and Regulatory Scrutiny (PFAS): The industry faces intense regulatory challenges (e.g., EU RoHS and REACH) due to the use of hazardous substances, particularly Per- and Polyfluoroalkyl Substances (PFAS), which are critical in semiconductor processes. This mandates costly investment in sustainable, "green chemistry" alternatives.

Supply Chain Volatility: The market relies on highly complex, global, and often geographically concentrated supply chains. Geopolitical tensions, trade disputes, and natural disasters can severely disrupt the supply of critical materials.

Emerging Market Trends

Focus on Green and Sustainable Chemistry: The demand for PFAS-free, low-toxicity, and recyclable chemicals is rising. Manufacturers are prioritizing R&D into bio-based and environmentally benign materials to meet regulatory requirements and corporate sustainability goals.

Advanced Packaging and 3D Integration: The shift toward advanced packaging solutions like chiplet architecture and 3D stacking requires new materials (e.g., low-K dielectrics, advanced encapsulants) for wafer-level bonding and interconnections.

Digitalization and AI in Manufacturing: The use of AI and predictive analytics for real-time process control, chemical dosing optimization, and predictive maintenance in chemical supply systems is becoming a key factor in improving yield and reducing waste in fabrication plants.

Next-Generation Materials: Research into novel materials like nanomaterials, advanced polymers, and specialized gases is accelerating to enable the next wave of flexible electronics, memory technologies, and quantum computing devices.

Browse More Reports:

Global Baobab Ingredient Market

Global Radiofrequency (RF) Microneedling Market

Global Radio Immunoassay (RIA) Reagents and Devices Market

Global Robotic Endoscopy Devices Market

Global GAN Epitaxial Wafers Market

Global Agave Spirits Market

Global Almond Powder Market

Global Anal Cancer Drug Market

Global Atherectomy Systems Market

Global Bejel Treatment Market

Global Biomimetic Nanocarrier Drug Market

Global Chemiluminescence Analyzer (CLA) Market

Global Cloud Seeding System Market

Global Commercial Boiler Market

Global Compostable Multilayer Films Market

Conclusion

The Global Electronic Chemicals and Materials Market is a highly specialized, capital-intensive, and strategically vital sector. Its growth is intrinsically linked to the relentless pace of technological scaling and the global surge in demand for sophisticated electronics. Future success will depend on industry leaders' ability to invest heavily in ultra-pure material innovation, navigate complex geopolitical supply risks, and meet increasingly stringent sustainability and regulatory mandates.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com